The Evolution of KYC

KYC is a fundamental regulatory requirement aimed at preventing money laundering, fraud, and identity theft. Historically, KYC involved manual verification processes that required customers to submit physical documents, leading to delays and potential errors. The advent of digital KYC has transformed this space, enabling faster, more accurate, and seamless verification processes.

Neokred's Vision and Approach

Neokred is at the forefront of this digital transformation, offering cutting-edge solutions that simplify and streamline KYC procedures. Their approach is rooted in leveraging advanced technologies such as artificial intelligence (AI), machine learning (ML), and blockchain to create a secure, efficient, and user-friendly KYC process.

“In a world older and more complete than ours they move finished and complete, gifted with extensions of the senses we have lost or never attained, living by voices we shall never hear.”

Rohith Reji, CEO

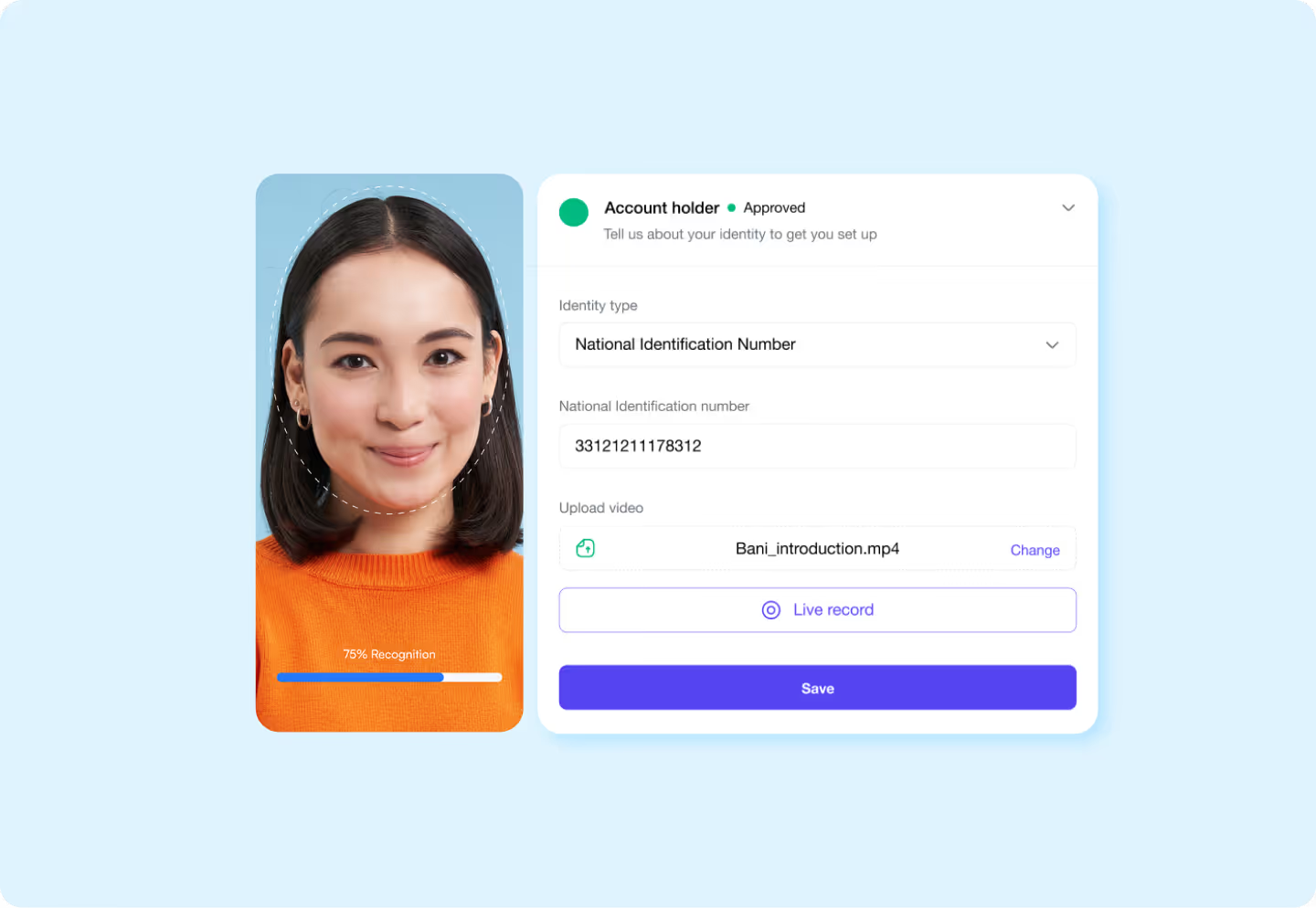

Key Features of Neokred's Digital KYC Solution

- AI-Driven Verification

Neokred uses sophisticated AI algorithms to verify customer identities in real-time. By analyzing patterns and detecting anomalies, AI ensures that only genuine documents are accepted, significantly reducing the risk of fraud. - Seamless User Experience

The platform is designed with the end-user in mind, offering an intuitive interface that guides customers through the verification process effortlessly. Users can upload documents, capture selfies, and complete verification steps from the comfort of their homes. - Blockchain Security

Blockchain technology enhances the security of KYC data by creating an immutable ledger that is resistant to tampering. This ensures that customer data is protected and can be audited with transparency.

Success Stories

Several businesses have already reaped the benefits of Neokred's innovative KYC solution. For instance, fintech startups have been able to onboard new users within minutes, while traditional banks have significantly reduced their KYC processing times and costs. The positive impact on customer satisfaction and operational efficiency has been profound, demonstrating the transformative power of Neokred's technology.

The Future of KYC with Neokred

As digital transformation continues to reshape the financial industry, Neokred is poised to lead the charge in KYC innovation. The company is continually refining its technologies, exploring new applications for AI and blockchain, and expanding its global footprint. With a commitment to excellence and a vision for a secure, efficient, and customer-centric KYC process, Neokred is setting new standards in the industry.

Conclusion

Neokred's digital KYC solution represents a significant leap forward in the way businesses approach identity verification. By harnessing the power of AI, blockchain, and seamless integration, Neokred not only simplifies the KYC process but also enhances security and compliance. For businesses looking to stay ahead in a competitive market, embracing Neokred's innovation could be the key to unlocking greater efficiency, cost savings, and customer satisfaction.

Conclusion

FAQs

Yes, you can try us for free for 30 days. If you want, we’ll provide you with a free, personalized 30-minute onboarding call to get you up and running as soon as possible.

Yes, you can try us for free for 30 days. If you want, we’ll provide you with a free, personalized 30-minute onboarding call to get you up and running as soon as possible.

Yes, you can try us for free for 30 days. If you want, we’ll provide you with a free, personalized 30-minute onboarding call to get you up and running as soon as possible.

Yes, you can try us for free for 30 days. If you want, we’ll provide you with a free, personalized 30-minute onboarding call to get you up and running as soon as possible.

Yes, you can try us for free for 30 days. If you want, we’ll provide you with a free, personalized 30-minute onboarding call to get you up and running as soon as possible.

Yes, you can try us for free for 30 days. If you want, we’ll provide you with a free, personalized 30-minute onboarding call to get you up and running as soon as possible.